Transaction Center

Time to bring it home. Find zipForm®, transaction tools, and all the closing resources you'll need. Except for the champagne — that's on you.

View the latest sales and price numbers. Find out where sales will be in upcoming months.

Get a roundup of weekly economic and market news that matters to real estate and your business.

Gain insights through interactive dashboards and downloadable infographic reports.

All Shareable Reports All Interactive DashboardsCatch up with the latest outreaches and webinars by the Research and Economics team.

C.A.R. conducts survey research with members and consumers on a regular basis to get a better understanding of the housing market and the real estate industry.

California Model MLS Rules, Issues Briefing Papers, and other articles and materials related to MLS policy.

Looking for information on how to file an interboard arbitration complaint? You've come to the right place! Find the rules, timeline and filing documents here.

Summaries and photos of California REALTORS® who violated the Code of Ethics and were disciplined with a fine, letter of reprimand, suspension, or expulsion.

The most recent edition of the Code of Ethics and Standards of Practice of the National Association of REALTORS® along with other important links to NAR information.

The California Professional Standards Reference Manual, Local Association Forms, NAR materials and other materials related to Code of Ethics enforcement and arbitration.

C.A.R. advocates for REALTOR® issues in Washington D.C., Sacramento and in city and county governments throughout California.

CREPAC, LCRC, IMPAC, ALF and the RAF comprise C.A.R.'s political fundraising arm.

The RAA: Protecting REALTORS® and Homeownership REALTOR® Action FundC.A.R. Senior Vice President Sanjay Wagle sits down with former Senate Majority Leader Emeritus Robert Hertzberg to discuss the proposed Middle-Class Homeownership and Family Home Construction Act.

Learn how you can make a difference, by getting involved yourself or by passing along valuable information to your clients.

|

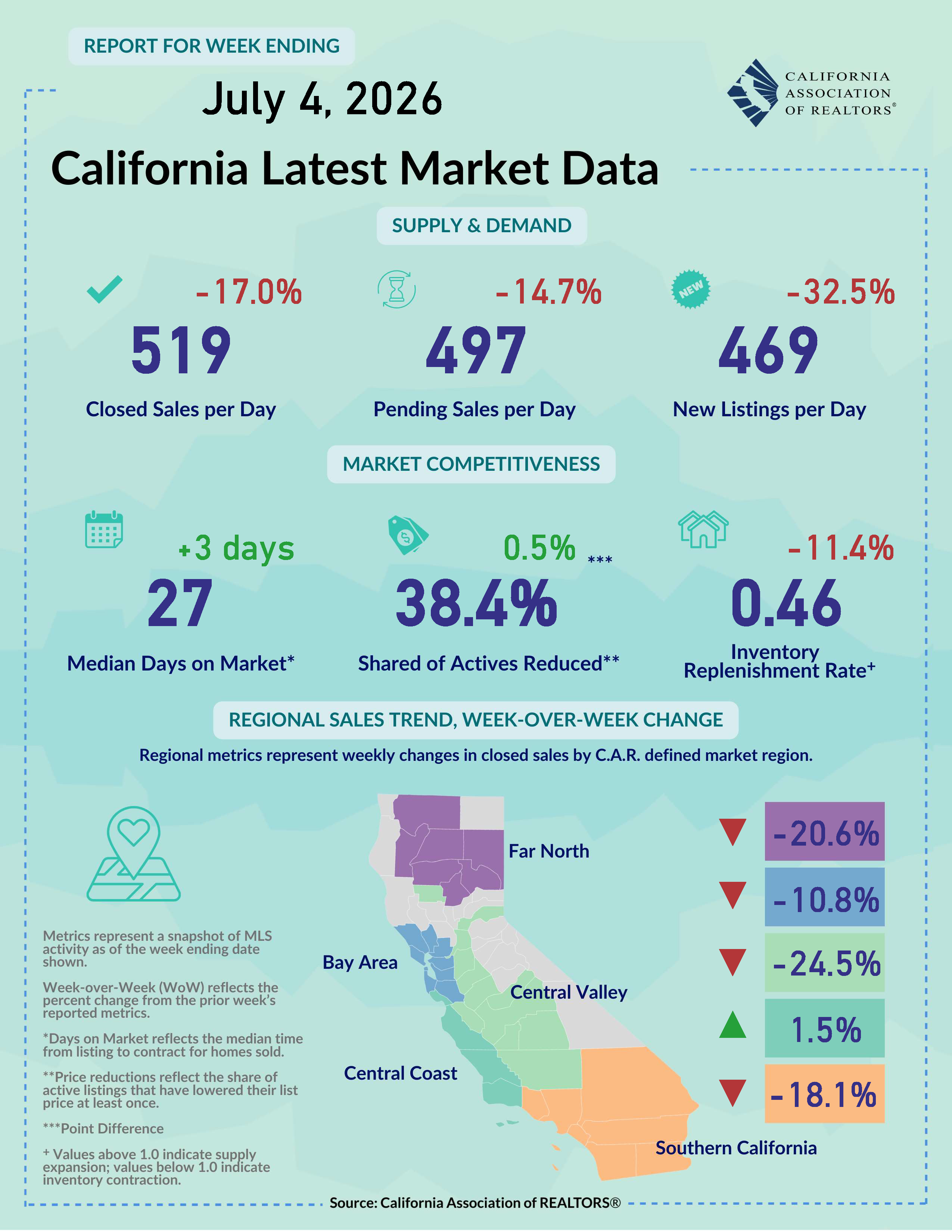

July 6, 2026 - Recent economic and housing data offer some encouraging signs for the outlook in the second half of 2026. Job growth has slowed but remains positive, consumer confidence is bouncing back, rental conditions are gradually firming, and residential construction could gain momentum if inflation eases and mortgage rates stabilize. These developments suggest the outlook remains cautiously positive, particularly as homebuying expectations have improved and parts of the California rental market continue to strengthen. However, headwinds remain and several challenges could temper the pace of improvement. Persistent affordability issues, soft labor-market conditions, stock market volatility, and lingering inflationary concerns are risks that could weigh on consumer demand and housing activity in the months ahead. U.S. economy adds fewer jobs than expected: U.S. job growth posted a monthly gain for the fourth straight month, but the increase was lower than expected. Nonfarm payrolls rose a seasonally adjusted 57k in June, the slowest growth pace in the last four months. May and April’s job figures were also revised downward, with employment growth updated to 129k and 148k, respectively. Despite the smaller increases, the economy still added 92k jobs on average per month over the first six months of the year. The health care and social assistance sector contributed the most to last month’s job growth, but health care employment gain appears to be slowing down. Leisure and hospitality, which surged in May, pulled back in June with a drop of 61k last month. In particular, hirings at restaurants/bars dropped 32.9k in June, bucking the expectation for a boost in employment in the sector fueled by the World Cup soccer tournament. The unemployment rate declined to 4.2% but the one-point dip was due largely to more people leaving the work force. Average hourly earnings increased 3.5% from a year ago but the increase remained below the annual inflation gain of 4.2%. With price growth outpacing wage growth, consumers will likely spend less in coming months if their pay increases continue to lag behind inflation. Consumer confidence improves with more expected to buy a home in the next six months: The U.S. Consumer Confidence Index inched up by 0.6 points in June to 91.2 from a downwardly revised 90.6 in May, according to the Conference Board. News of a ceasefire agreement between the U.S. and Iran, along with moderations in gas prices, help elevate confidence marginally in June. While consumers remained concerned about the present situation – as the May’s index dropped three points from the prior month, their short-term outlook improved as the expectation index rose three points last month. Americans’ perception of the job market, however, continued to be soft as 22.5% of them said jobs were “hard to get,” an increase from the month before and the level was the highest since January 2021. Homebuying expectations improved on a six-month rolling basis, despite 61.5% of the respondents expecting higher interest rates over the next six months. With employment concerns likely to linger on in the near term, consumer confidence should still improve further in coming months but at a gradual pace. Rental market continues to improve slowly: Housing demand in the apartment rental market is slowly growing during the busy summer season but overall conditions in the sector remain relatively cool. The national median rent in June increased 0.4% month-over-month to $1,385, inching up for the fifth consecutive month since February. On a year-over-year basis, median rent remained below last year’s level with a decline of 1.2%, the smallest dip in the last six months. Despite an increase from the prior month, the national median rent remained below its recent high set in August 2022 by 4%. Meanwhile, the average national vacancy rate for multifamily homes trended down to 7.2% after hitting its latest high at 7.3% in February. List-to-lease time, albeit remaining elevated, ticked down to 29.7 days and reached the lowest level in 10 months. At the metro level, three areas in California were on the top 10 fastest year-over-year rent growth list in the U.S., with San Francisco (7.4%) and San Jose (6.1%) taking the top two spots, while Fresno (2.3%) came in at number 9. With housing affordability remaining a challenge for many would-be buyers, recovery in the rental market will likely continue to progress slowly for the rest of the year. Residential construction up in May due primarily to home improvement: U.S. construction spending inched up in May from April but remained below last year’s level, according to the latest monthly report released by the Commerce Department. Total outlays reached $2.210 billion in May, up 0.1% from April’s $2,207 billion but down 1.5% from May 2025. Residential construction climbed again on a month-over-month basis for the third time in a row and was up 1.8% from last May. The increase was driven primarily by remodeling, which posted an 8.1% gain from 12 months ago. May’s new single-family construction declined 4% from a year ago but new multifamily went up 3.3% year-over-year. With geopolitical risks subsiding while the rental market showing signs of improvement, building activity could pick up in the second half of 2026 once inflation starts calming down and mortgage rates begin to stabilize. Young adults have difficulty entering homeownership as home prices grow faster than income: A recent Pew Research Center analysis found that homeownership has become significantly less attainable for young adults under age 40, with nearly 89% saying it is harder to buy a home today than it was for their parents’ generation. Since 2019, inflation-adjusted U.S. home values have increased 30%, while incomes for households headed by adults under 40 have risen just 9%, pushing the national home price-to-income ratio from 2.9 to 3.5—the highest level since 2006. Home values outpaced income growth in 142 of the 160 metro areas studied. The findings are especially concerning for California, as nine of the ten most unaffordable metro areas are in California. The study underscores the continuing affordability challenges facing California households, where rapid home price appreciation has far outpaced income growth, making it increasingly difficult for younger generations to transition from renting to homeownership. Note: This summary report gets updated every Monday by 6:00 pm PST. Feel free to email us at [email protected] if you have any questions and/or feedback.

|

|